Aging Energized Articles

Read about topics to help you age well, enjoy your retirement years, and navigate the intricacies of Medicare and Social Security.

Will You Age in Place or at a Multi-Functional Living Location?

If you are healthy and fully functional on your own, now is the time to give this serious consideration.

The best answer may be to age in place as long as feasible and then move into a multi-functional living location. The problem is you and your adult children may not agree on when is the best or most appropriate time to make this type of move, if ever. Your best defense is a good offense. Get out in front of this and plan for what is best for you and/or your spouse now.

First, let’s define our two terms. “Age in place” means you will continue to live in your home and when the time comes that you need help with activities of daily living, you will have someone come to your home to help you and provide these services.

To move into a “multi-functional living location” means you will live in an apartment at a location where three stages of care are provided. The first stage is independent living where the primary “care” provided is daily meals and weekly house cleaning. At this same l...

Do You Have a Plan for Long-Term Care?

This topic is important because Medicare doesn't cover long-term care. Never has, never will.

Medicare Isn't the Answer

Medicare only covers medical issues, not what is called "Activities of daily living." As we decline and need extra help and care, Medicare isn't the answer.

What is the answer? Fundamentally there are three answers

- Long term care insurance.

- Pay your own way with existing financial resources from yourself or other family members.

- Medicaid for Seniors.

As we decline, the help we need may start off simply as needing help with food preparation, getting dressed each day, bathing, mobility (help getting in and out of a car). As time goes on, our needs often increase beyond the capability or capacity of our loved ones who are happy to help but have lives of their own to live, or they may be many miles away and cannot help everyday or on a regular basis.

This is where we come back to the central question: Do you have a plan for long term care? Have you specificall...

Tax Friendly States for Retirees

Are you curious about which states have the most tax-friendly treatment for retired people? This handy map shows you which states are most tax-friendly, mixed, and least tax-friendly. Where does your state rank? You may be inclined to move after looking at the map.

Once you're looking at the handy map you can click on each state and drill into more detailed information or select the state for comparing up to 5 states in a compare list. You can also click on links to get detailed information about the 10 most tax-friendly and 10 least tax-friendly states for retirees.

The TOP 4 Medicare Cost Increases for 2021 Every Medicare Recipient Needs to Understand

Every Medicare recipient wants to understand their costs, especially when they go up each year. On November 6, 2020, the Centers for Medicare & Medicaid Services (CMS) announced its price increases for 2021. Here are four Medicare cost increases taking effect January 1, 2021 that you need to be aware of and understand.

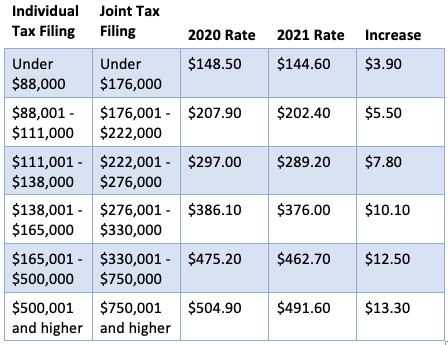

1. Medicare Part B Premium

The cost increase Medicare recipients are most interested in is Part B's monthly premium. For 2021, the base rate is increasing from $144.60 in 2020 to $148.50 in 2021. This is an increase of 2.6%, and only increases the Part B premium by $3.90 per month. But if you're retired and on a fixed income, such as Social Security (which is only increasing 1.3% in 2021), this is probably not a welcome increase.

Monthly Rate Increases by Income Level

If you earn over $88,000 per year as a single, or $176,000 for married filing jointly, rates are going up based on your income level, as shown in the table below.

2. Medicare Part B Deductible

Medic...

Aging Well, Just Like Springsteen

At the very young age of 71, Bruce Springsteen has released his latest album, Letter to You, and a film of the same name that records the making of the album.

Many of the songs are about growing older and death. Yet in his article Bruce Springsteen and the Art of Aging Well in The Atlantic, author David Brooks calls the album "both youthful--loud and hard-charging--and serene and wise." Brooks also says "Letter to You is rich in lessons for those who want to know what successful aging looks like."

Active aging is now a decades-long phase of life. According to the International Council on Active Aging, it embodies fully engaging in life within all seven dimensions of wellness:

- Emotional - the ability to be aware of and direct your feelings helps to create balance in life.

- Environmental - bringing people into the natural environment and encouraging active living through urban and property designs emphasizing walking paths, meditation, and vegetable gardens.

- Intellectual/cognitive ...

Social Security 2021 COLA Increase Announced

The Social Security Administration just announced a 2021 cost-of-living adjustment (COLA) of 1.3%. From the Social Security Administration's website:

"The 1.3 percent cost-of-living adjustment (COLA) will begin with benefits payable to more than 64 million Social Security beneficiaries in January 2021."

COLAs are implemented automatically based on the annual increase in consumer prices. This has been happening automatically since 1975, when legislation from 1972 took effect. Since that time, Social Security beneficiaries don't have to wait for a special act of Congress to receive a benefit increase.

Other Changes

There are a few other changes. They include:

- The maximum amount of earnings subject to the Social Security tax will increase to $142,800.

- The earnings limit for workers younger than full retirement age (FRA) will increase to $18,960. The Social Security Administration deducts $1 from benefits for each $2 earned over $18,960.

- The earnings limit for people reaching ...

New Book--Social Security Basics!

Social Security is probably the most complex area to understand and navigate for pre-retirees and retirees. Compared with Medicare, it certainly has the most moving parts, nuances, and unique situations, which is saying a lot because Medicare is also quite complex.

Our newest book, Social Security Basics, provides the information you need to make an informed decision about when (at what age) to start collecting Social Security benefits. It's the most asked question—and hardest to answer—about Social Security. We do our best to cover all the angles to provide you with the confidence you need to make this all-important decision. This includes addressing whether you should consider collecting Social Security benefits early, before your full retirement age.

We also cover some specific topics that impact a significant number of people. They include:

- Spousal benefits.

- Survivor benefits.

- People often have questions about Social Security benefits being taxed, so we tackle this topic.

- A ...

New Book--Medicaid for Seniors Basics

It's launch time again! We're super excited to release our newest book, Medicaid for Seniors Basics. It explains how the Medicaid for seniors program for long-term care can help those who have a low in come and have exhausted their assets can pay for the long-term care they need.

It explains the income and asset requirements, how the non-applying spouse is affected, and important concepts such as:

- 5-year look back

- Spend down

This book can be your lifeline to paying for essential care for yourself or a loved one.

You can find this book in the Aging Energized shop.

Social Security Basics -- New Course!

We are very excited to announce the launch of our third course, Social Security Basics. As you're planning your retirement, understanding how Social Security works is key to knowing what your financial situation will look like. Decisions you make about when you start collecting Social Security benefits impact how much you'll receive each month. You can retire as early as age 62 and collect less than your full retirement age, or you can wait until age 70 and collect more. Understanding how this works is key to knowing when to make the leap into retirement.

The course covers many other topics, including spousal benefits (if you're divorced, did you know you may be entitle to collecting Social Security benefits based on your ex-spouse's earning history?), survivor benefits, tax considerations, how to apply for social security benefits, and much more.

The course is simple and straight forward. It includes 7 video lessons, each with a handy download summarizing what's included in the cou...

Medicare vs. Medicaid - Do You Know the Difference?

Medicare and Medicaid sound similar, but they're actually very different. Each provides different types of assistance to help with healthcare. Both are government programs, but they are very different. Medicare is provided by the federal government (the Social Security Administration). Medicaid is provided by state governments and varies from state to state. Medicare is available to anyone age 65 and older who has worked at least 10 years in the U.S., and at any age to people with disabilities. Medicaid is only available to people with limited income and assets.

Let's look at the other differences.

Medicare

Medicare is federal healthcare insurance for people 65 years of age or older. You can get Medicare under age 65 if you have a qualifying disability, including end stage renal disease (ESRD) or ALS. Medicare covers inpatient or hospital care (Part A), outpatient services (Part B), and prescription drugs (Part D). Other plans, such as Medicare Advantage (Part C) and Medigap are als...